Main issues are chip shortage and inflationary pressures

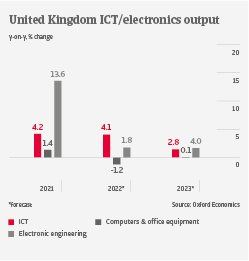

ICT sales in the United Kingdom grew strongly in 2020 and 2021, mainly driven by a sharp increase in remote working and e-learning. Growth is set to continue in 2022, as businesses invest in upgrading their IT-infrastructure. However, in many cases supply has not been able to keep pace with demand. Supply shortages of semiconductors remain a serious issue, and backlogs remain significant along the ICT value chain, hampering production. Meanwhile smartphone manufacturers have run out of their stockpiles of chips, and game consoles are in short supply. Duplicated chip orders by ICT producers don’t help the backlogs. Inflationary pressures, increased transport costs, and strong market competition additionally affect the business performance.

As the ongoing supply chain issues meet persistent demand, most end customers are willing to accept price increases. Therefore, we expect profit margins of ICT businesses will remain stable in the coming months. However, ICT sales to consumers could reduce in the coming months as high food and energy prices affect the purchasing power of households. Additionally, after the expiry of lockdowns, consumer spending has shifted back towards social activities and travel.

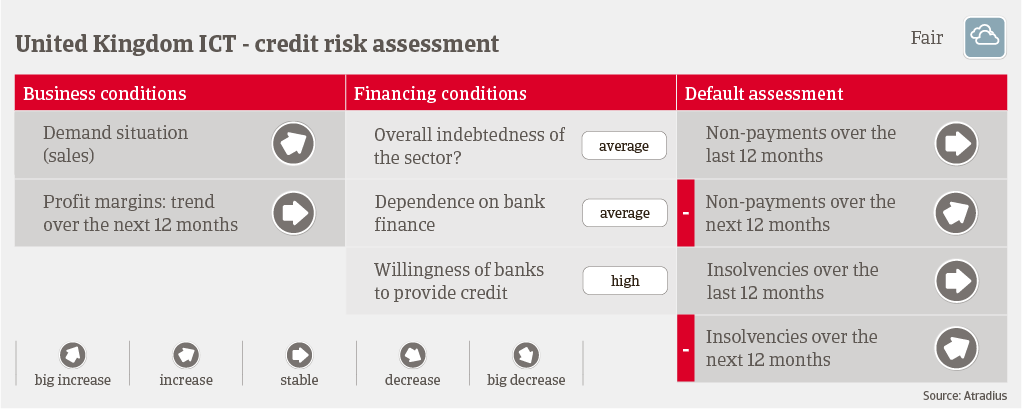

Payments in the British ICT industry take 60 days on average. Payment behavior has been good during the past two years, and the number of payment delays and insolvencies was low in 2021 and H1 of 2022. However, we expect both to increase in the coming months as government support measures expire, and the number will return to “normal” levels seen in 2019. Businesses in the managed print segment could be particularly affected after suffering from deteriorating sales during the pandemic. Additionally, data centres face increased inflationary pressures.

Our underwriting stance is rather selective for the managed print segment (case-by-case approach). We are generally open for all other subsectors because ICT has proved to be resilient, with a lower credit risk compared to most other industries. The long-term growth prospects are benign, supported by a flexible business environment, world-class universities, and a strong digital services economy in the UK.

Свързани документи

986KB PDF