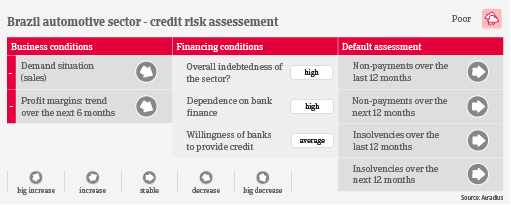

Economic uncertainty hinders external financing for automotive businesses

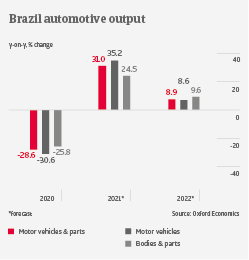

In H1 of 2021, new passenger car registrations increased 33% year-on-year, but were still 18% lower than in H1 of 2019. Subdued consumer sentiment and high unemployment had a negative impact on sales and margins. That said, automotive businesses active in the commercial vehicle/truck segment benefited from increased demand (e.g. from agriculture and e-commerce companies), leading to revenue growth and higher profitability compared to their peers in the passenger car segment.

Semiconductor shortage, higher inflation and expenses for restructuring have put pressure on the profitability of automotive businesses, resulting in higher credit risk. While the weaker currency exchange rate helps exporters, it has increased import prices for chips and other materials, negatively affecting operating costs.

Performance in the coming months will remain impacted by the lack of semiconductors and elevated input costs, while idle capacity will remain high. At the same time, the renewal of a government scheme to reduce working hours and salaries should partially mitigate pressure on businesses' results.

Payments in the automotive industry take about 90 days on average. Currently it is expected that both payment delays and insolvencies will not increase sharply in the coming twelve months. Due to low cash generation, automotive businesses will rely even more on working capital lines to reinforce their cash position and to protect their liquidity. While Original Equipment Manufacturers (OEMs) and large Tier 1 businesses can count on intercompany loans from their parents abroad, most suppliers will continue to apply for bank loans. However, they could face difficulties in obtaining external financing, given the uncertain outlooks for the Brazilian economy and the sector performance.

For the time being, our sector assessment remains “Poor” and our underwriting stance rather restrictive. Downside risks remain for the industry, as it is highly dependent on the future interest rate development and related bank loan conditions, as well as on consumer confidence and household purchasing power.