The Covid-19 pandemic and the Russia-Ukraine war pose challenges to global value chains.

- The Covid-19 pandemic and more recently the Russia-Ukraine war have posed unprecedented challenges to global value chains. Demand and supply side shocks have created several bottlenecks along the supply chain, ranging from logistical disruptions, to shortage in equipment and labour, as well as intermediate inputs such as semiconductors.

- Despite the challenges, we do not expect a major step back on the globalisation ladder. The key economic rationale for value chains – labour cost arbitrage, i.e. firms moving production to locations with relatively cheap labour - still holds. Furthermore, countries are not necessarily better off by taking an alternative strategy.

- We argue that alternatives, such as diversification of suppliers or customers, or the reshoring of production, also come with important downsides, and they do not necessarily increase robustness or resilience.

Covid hits value chains

The Covid-19 pandemic hit the world economy as a surprise shock. The pandemic created strong disruptions along the global value chain (GVC) and by doing so laid bare some vulnerabilities of global production networks. The value chain disruptions that emerged during the pandemic have both demand and supply-side causes. The Russia-Ukraine conflict has exacerbated already existing disruptions. It pushed up commodities prices and distorted parts of the European value chain, especially in the automotive sector.

On the supply side, production was hit in the early stages of the pandemic by factory shutdowns in China. This took place in January/February 2020. Given the central place of China in GVCs, this had an immediate effect on the global production in manufactured goods. When Chinese production recovered in the spring of 2020, the pandemic moved to Europe and the US, leading to factory shutdowns there, and ‘reinfecting’ Chinese industry, as inputs from the US and Europe were more difficult to source. Global production started to pick up in the second half of 2020 as economies learned to adopt to the virus and restrictions were scaled down. In Q4 of 2020, global production had already recovered to its pre-pandemic level. Occasionally factories still shut down, especially in China, which has adopted a ‘zero Covid’ strategy. However, global production levels suggest that the manufacturing industry is relatively resilient to new waves of infections.

On the demand side, there was a fall in global demand at the start of the pandemic as uncertainty soared, disposable incomes declined, and there were practical barriers to consumption, such as store closures. Since the second half of 2020, however, demand has returned as economies reopened, households started to draw down their excess savings and governments implemented fiscal stimulus. Consumption patterns also shifted from (local) services to (imported) manufactured goods, such as electronic products and equipment, partially related to working from home. This triggered higher demand for merchandise trade, creating logistical disruptions in the transport sector. Shipping costs soared (figure 1) due to the misallocation of shipping containers, and several ports had problems processing cargo due to a shortage of dockworkers and truck drivers. One of the worst affected harbours is Los Angeles-Long Beach, where the number of container ships waiting ‘at anchor’ rose to record-high levels in January 2022. Looking at the global picture, the situation has not become a lot better in recent months.

The surge in demand for industrial goods demand has resulted in a sharper than usual drawdown of inventories relative to demand. Inventory levels are still below historic averages, but there is evidence that inventory tightness in recent months is easing in several sectors. One exception is the semiconductor industry, which is still experiencing high orders amid already tight capacity. The shortage in semiconductors is primarily demand-led, triggered by a rapid rebound of vehicle sales and a lockdown-driven boom in electronics products for which semiconductors are important inputs.

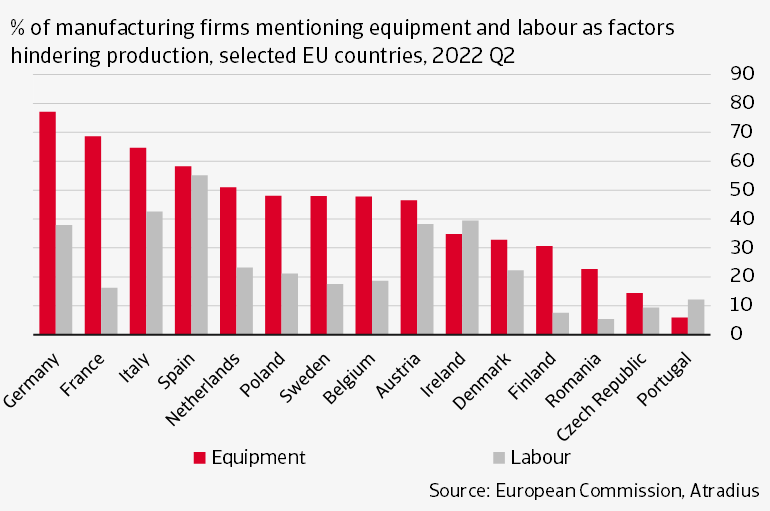

Even outside of semiconductor-dependent industries, firms have been experiencing equipment or material shortages. In Q2 2022, a record 51% of EU manufacturing firms reported equipment as a factor limiting production, with this number as high as 77% in Germany (Figure 2). In the US, companies are also reporting a shortage of physical inputs The outbreak of the Russia-Ukraine war has exacerbated existing supply chain distortions and volatility in commodities prices. Despite being only partially integrated in the European supply chain, Russia and Ukraine provide some key manufacturing inputs. This impact is being felt particularly in the automotive industry, with some car manufacturers limiting or shutting down production. Ukraine is a key producer of various scarce metals such as palladium (used in catalytic converters) and neon (used in lasers for the manufacture of microchips).

Similarly, labour shortages are also a key risk for the industrial recovery in both the EU and the US. In Germany, where many jobs were saved thanks to the government’s furlough scheme, manufacturing employment has not recovered from the 2020 dip (despite strong demand). 38% of German manufacturing firms are experiencing labour shortages, compared to 28% in the EU as a whole.

Disruptions to resolve gradually

Our current expectation is that supply chain disruptions will resolve only gradually. We expect that it will take well 2023 to allocate shipping containers to the right places, keeping shipping costs high in the near term. The semiconductor shortage is also expected to continue in 2022. Recent data suggests the chip shortage has passed its peak as major chipmakers in Asia are ramping up production. What could also help is that consumers have started to rotate back from goods consumption towards services. But it is likely to take well into 2023 for the semiconductor shortages to disappear.

Post-financial crisis trends in global value chains

The Covid-19 pandemic arrived at a time when the major driving forces of international production were already at an inflection point. For several decades after the 1980s, global manufacturing processes have exploded thanks to low trade costs enabled by the trade agreements and dramatically lower transportation costs. In addition, information and communication technology reduced communication costs. As a result, global value chains have started to play an increasingly important role in global production. China’s participation in the global economy is probably the most noteworthy GVC trend of the past three decades. In 1990, Germany, the United States, and Japan were the three central nodes connecting cross-continent trade flows. China was a tiny dot with very low participation in GVCs. However, by 2019 China had replaced Japan as the central node in Asia and replaced the United States as the second-largest GVC hub globally (Germany being first).

After the 2008/2009 financial crisis, however, the growth momentum for international production has stalled. Many of the potential benefits of globalisation arising from differences in labour costs and productivity have already been exploited. On the policy side, the pendulum started to swing from liberal trade toward more interventionism in national economic policies and a return of protectionism. The US-China trade war, which emerged under the presidency of Donald Trump, is a good example of this trend. On some measures globalisation is indeed levelling off. World exports as a share of GDP has remained more or less constant since 2008. For the US and China, we observe that the share of exports in GDP has stagnated or declined somewhat since 2008. For Germany, however, such a decrease is not visible.

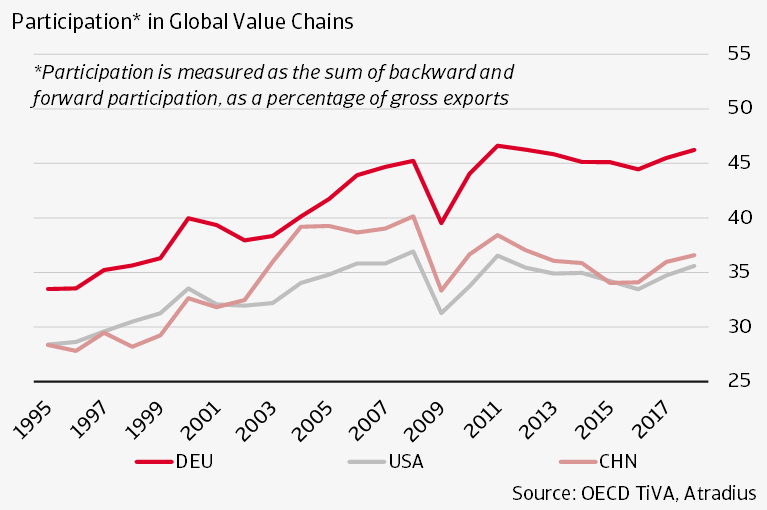

On another measure, that of the participation in global value chains, we see some stagnation for the US and China but no major reversal (see figure 3). There is only data available until 2018 and unfortunately not for the full period of the US-China trade war and the pandemic. There was a dip in GVC participation in 2009, due to the ‘Great Recession’ that followed the financial crisis, but this was followed by a recovery in later years. In 2018, it remained high on average, but the plateauing suggests that most of the gains from globalisation have been reaped.

Covid-19 and Russia-Ukraine conflict as such no game changers to GVC participation

The Covid-19 pandemic and more recently the Russia-Ukraine war has posed challenges to GVCs. The stark fall in trade in the early months of the pandemic reflected the confluence of pandemic-induced demand and supply shocks. The reopening of economies, mainly since the second half of 2020, created such a strong demand for goods that new bottlenecks emerged. Many firms, both multinational corporations and small local suppliers, have been negatively affected by the bottlenecks. In surveys held after the Covid-19 outbreak, the chief executives of large firms and multinationals expressed the belief that it will take years for business activities to return to pre-crisis levels.

Covid-19 and the Russia-Ukraine conflict are providing fresh fuel to the pre-existing debate on whether GVCs have become too vulnerable to shocks. Some economists foresee little significant change in the way that GVCs are shaped, because the economic rationales continues to hold. GVCs have brought many benefits by allowing firms to source their inputs more efficiently, to access knowledge and capital beyond the domestic economy and to expand their activities into new markets. Others believe that Covid-19 has become a wake-up call for a new risk-reward balance for GVCs. Firms may consider several options to improve supply chain resilience, including reshoring production, diversifying suppliers and holding more inventory.

The first option is reshoring or nearshoring. This is probably the most drastic trajectory. It challenges the most defining elements of GVCs - the fragmentation of tasks and geographic dispersion – and is associated with lower GDP and incomes as fewer efficiency gains can be exploited. The key drivers for reshoring could be the policy environment (push for higher degree of self-reliance post-pandemic) and the possibly to automise parts of the production process, which lowers the relevance of labour cost arbitrage opportunities. Labour cost arbitrage is the practice of moving production to locations where labour is cheaper. There could be strategic considerations to nearshore production. For instance, in critical sectors like energy, sensitive technology, food supplies, medical equipment, we may see more nearshoring or onshoring.

However, it is important to note that localised production is not necessarily less vulnerable to shocks. Looking at the situation of a global pandemic, almost every economy is affected by both supply and demand shocks, although to different degrees. This means that reshored production can also be affected by lockdowns. Moreover, shocks of a different nature, such as production accidents, natural disasters and financial risks, can happen in any location, so that local production is no guarantee for robust value chains. On the contrary, during the Covid pandemic, value chains were even able to address shortages in the supply of essential medical goods. For instance, in South Korea a new industry emerged that exports millions of Covid-19 test kits to more than 100 countries. This took place in a matter of months since the outbreak of the pandemic.

Could the war in Ukraine then be a major step toward deglobalisation? It will almost surely accelerate Russia’s reorientation to the East, to China, India, and to countries Central Asia. But trade volumes between these economic blocs remain relatively modest on a global scale. Moreover, Russia represents less than 2% of global GDP. It is unlikely that China will want to create a regional trade structure that might damage its trade relationship with advanced economies. Advanced regions are still China’s main outlet for manufactured goods and a source of key technologies. Trade with the US and its allies in Europe and Asia still represents over 70% of China's foreign trade, versus only 4% with Russia and India.

It is not evident that a shock like Covid-19 will lead to an acceleration of reshoring. Earlier important supply chain shocks, such as the 2011 earthquake in Japan, did not lead to reshoring or nearshoring of production as a response. Importers did, however, reduce reliance on Japan in favour of low-cost developing economies. We expect that in the wake of the Covid-19 crisis, reshoring seems a viable and likely option only for some high-tech industries prone to protectionist pressures. This can include essential goods – such as medical equipment - or goods that are strategically important from an economic or technological perspective (for example, automotive and electronics).

The second option is diversification of supply, a solution that leverages GVCs rather than dismantling them. Diversification of suppliers at the various steps of production in a value chain can increase robustness and resilience, as a negative shock hitting supplies from one location can be offset by substitute supplies from other locations. However, maintaining alternative suppliers imposes additional costs on firms, as they need to invest in multiple suppliers to tailor inputs and to make sure that parts and components from different manufacturers fit together. Certain industries, such as semiconductor manufacturing, are highly concentrated in a few countries, because significant upfront investment in production limits the number of suppliers. If this is the case, diversification of input supply will be more difficult.

Digitalisation of the supply chain is a key driver that could make diversification easier and less costly as it enhances the opportunities for coordination and control. Diversification is most likely in low-tech, low cost industries, such as textiles and apparel. In addition to low-tech industries, diversification also offers opportunities in service industries, particularly higher value added services.

Finally, holding more inventory probably is the most straightforward way to enhance robustness of GVCs. At the same time, this strategy also comes at a cost. Profit-oriented companies will be reluctant to hold excess inventory, because it ties up capital but also requires managing this inventory, warehousing it, maintaining it, and preventing damage or theft of it. In addition, many products can expire or become obsolete while they are stored in inventory. Although many firms boosted their inventories and stocked up on raw materials during the Covid-19 crisis, this development is unlikely to turn into a long-term trend.

We do not expect a major shift in production strategy following Covid-19 pandemic and the Russia-Ukraine conflict. It could lead to some strategic reorientation, but no major step back on the globalisation ladder. The most important argument is that the key rationale of global value chains – labour cost arbitrage opportunities – still holds and the alternatives to GVCs are not necessarily better. Instead, we think it is more likely that firms will make slight adjustments to their production strategies. For instance, by maintaining higher inventories of critical goods, such as medical supplies. There may be limited reshoring as labour costs in some manufacturing hubs, notably China, increase as they move up in the value chain, but this would have happened irrespective of the current supply chain bottlenecks. Our belief that the key economic rationale for global value chains continues to hold is corroborated by experience with previous supply chain shocks, such as during the 2008/2009 financial crisis and the 2011 Japan earthquake.

Theo Smid, Senior Economist

theo.smid@atradius.com

+31 20 553 2169

Свързани документи

196KB PDF