The shift to e-mobility is a major challenge for many suppliers

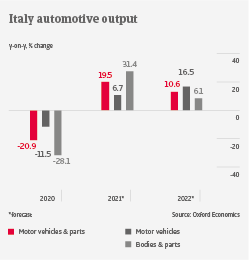

Italian car production already decreased in H2 of 2018 and in 2019, with a major 20% contraction in 2020 due to the pandemic. While it rebounded in H1 of 2021, production has slowed down again since Q3, mainly due to semiconductor shortages, and is expected to contract 2% this year. After the merger of PSA and FCA to Stellantis a restructuring process is underway in the industry to create synergies and savings, which could impact the future of several car plants in Italy.

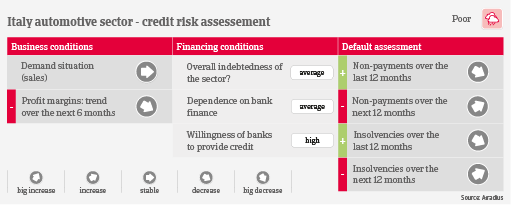

Disruptions in car manufacturing (e.g. “stop-and-go” production) have a negative impact on the whole supply chain. Many suppliers additionally suffer from increased raw material costs (e.g. for steel, plastics and resin) and higher energy prices. Profit margins of Tier 2 & 3 businesses have started to deteriorate due to lower revenues and higher production costs, while most Tier 1 suppliers still show good solvency and acceptable gearing.

Payments in the industry take 75 days on average, and payment behaviour returned to normal levels in early 2021 after a deterioration in 2020. It is expected that automotive insolvencies will increase by about 5%-10% in the coming twelve months, mainly affecting smaller suppliers that suffer from production disruptions and higher input costs. Another issue is the expiry of government measures (e.g. bank loans with state guarantee). The number of business failures could be even higher, if semiconductor shortage and production shortfalls last in 2022.

Due to the production disruptions, modest rebound in short-term demand and the elevated credit risk amid suppliers, our underwriting stance remains rather restrictive. Regarding e-mobility, the current government schemes for electric cars (Ecobonus) are only temporary and rather insufficient to boost sales. At the same time, many Italian suppliers show a technological gap compared to their European peers. It is expected that stronger businesses will be able invest and reconvert their plants towards e-mobility, while other suppliers will have to leave the market in the coming years.