Increase in production of primary products planned to lower reliance on China

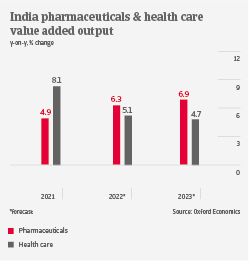

Indian pharmaceuticals value added output is forecast to grow more than 6% annually in 2022 and in 2023, due to the ongoing rollout of Covid-19 vaccinations, a rebound in non-Covid related medical treatments and a surge in generic drug exports. However, in H1 of 2022 drug producers still face pressure on gross margins, due to high commodity and transport costs. Domestic wholesalers and pharmacies continue to generate low, but stable margins.

While generic drugs still account for about 70% of output, the pandemic has spurred Indian drug producers to substantially increase their R&D spending. Due to a serious supply disruption in 2020, Indian drug producers intend to increase local production of Active Pharmaceutical Ingredients (APIs) in order to reduce their reliance on Chinese deliveries. Those imports have meanwhile rebounded, but are not yet back to pre-pandemic levels. The government has announced a large incentive scheme (e.g. with tax exemptions) to boost local API production, which will last until 2030.

The industry is highly export-oriented, being one of the leading suppliers of generic drugs to the US. Exports could be impacted by resumption of US Food and Drug Administration (USFDA) inspections of Indian production plants. Failures to meet required quality standards could lead to lower sales to the US, and could have a negative effect on margins.

We expect the domestic drug market to grow steadily in the coming years, due to demographic trends and rising household income. The growing middle class can increasingly afford high quality drugs, while demand for treatments (and related drugs) of cardiovascular diseases and other chronic diseases will increase.

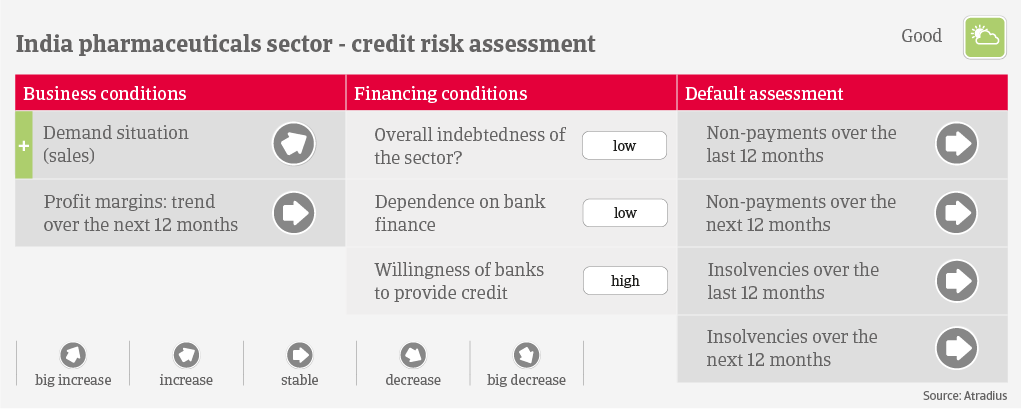

The balance sheets of most Indian pharmaceutical businesses and their capacity to generate cash are strong. Both gearing and dependence on bank finance are low. Payment behaviour has been good over the past two years, and we expect the number of protracted payments and business failures to remain low in 2022. Given the benign credit risk situation of most businesses and good growth prospects in the coming years, our underwriting stance is open for all segments.

Свързани документи

969.0KB PDF